Planning ahead for when you’re no longer here can be daunting. But it’s useful to know that if you die in retirement, your loved ones may be eligible to receive financial support as part of your pension benefits. The rules vary depending on your scheme, so we’ve put together a short summary to help you understand.

Choose your scheme below and see how your pension can give financial protection to your loved ones.

1. Death grant

This is a one-off lump sum your beneficiaries may receive. The death grant will be paid to them if you die before the age of 75 and within ten years of receiving your pension (or five years if you left the LGPS before 1 April 2008).

The amount they would receive is calculated depending on the date you retired:

Before 1 April 2008: the amount payable is five times the value of your annual pension, minus the amount that has already been paid to you.

On or after 1 April 2008: the amount payable is 10 times the value of your annual pension, minus the amount that has already been paid to you.

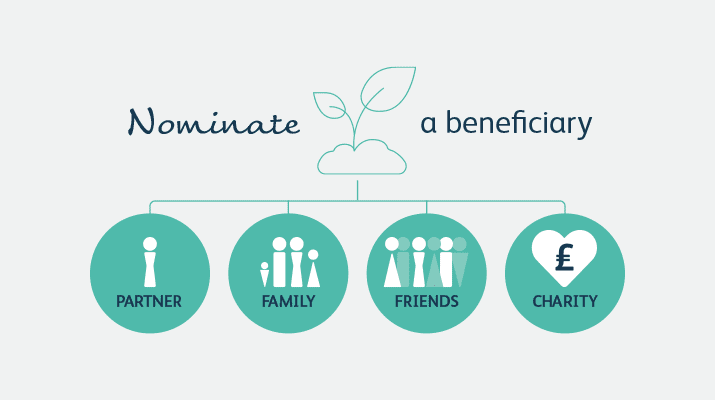

Nominating beneficiaries

Your pension fund has the power to decide who will receive the death grant but you can still nominate one or more beneficiaries (including charities) in your online PensionPoint account. Your pension fund would take your wishes into account when making their decision.

2. Survivor’s pension

As well as a death grant, your loved ones may be eligible to receive monthly pension payments if they qualify as your spouse, civil partner or cohabiting partner. This benefit would be paid to them for the rest of their life.

The amount they would receive is generally:

- 50% of benefits built up before 1 April 2008

- 37.5% of benefits built up between 1 April 2008 and 1 April 2014

- 30.625% of benefits built up on or after 1 April 2014

Please note – if you entered a marriage or civil partnership after leaving the LGPS, your surviving spouse or civil partner may receive a smaller amount.

Your cohabiting partner would only receive a survivor pension if you paid into the LGPS on or after 1 April 2008 and if your relationship meets certain criteria.

Plus, the amount they receive would only be based on the benefits you built up after 5 April 1988 (unless you paid extra contributions to cover earlier benefits).

3. Children’s pension

Your pension can provide financial security for your child(ren) if they meet certain qualifying conditions. Depending on their circumstances, children’s pensions are usually paid up to age 18 or age 23 if they are in full time education.

For more details, see the LGPS scheme guide.

1992 scheme

1. Survivor’s long term pension

If you die in retirement and have been a member of the scheme for at least two years, your loved ones may be eligible to receive a pension if they qualify as your surviving spouse or civil partner (excluding cohabiting partner). This would be paid to them for the rest of their life – unless their relationship status changes.

Their survivor’s pension would stop if they re-married or formed a new civil partnership (unless this took place after 1 April 2015 and you died because of an injury on duty or when travelling to or from work). Your Fire and Rescue Authority may also re-instate their pension in certain circumstances.

Your partner would receive around half your annual pension. But it could be less if you had been paying into your pension before April 1972 or your marriage/civil partnership took place after retirement.

2. Bereavement pension

In addition to a survivor’s pension, your surviving spouse or civil partner would receive a bereavement pension for the first 13 weeks after your death. If you don’t have a surviving spouse or partner, your child(ren) would be eligible. The amount is usually the difference between the survivor pension and your weekly rate of pension when you die.

3. Children’s pension

Your pension could also provide financial security for your child(ren) if they meet certain qualifying conditions. Depending on their circumstances, children’s pensions are usually paid up to age 18 or age 23 if they are in full time education.

For more details, please speak to your FRA or visit the LGA website.

2006/2006 Special Members/2015 scheme

If you die within five years of receiving your pension (before age 75), your beneficiaries may receive a one-off lump sum. This is known as a five-year guarantee period. The lump sum is calculated as five times your annual pension minus the amount of monthly payments already paid to you.

Nominating beneficiaries

Your Fire and Rescue Authority (FRA) has the power to decide who receives the death grant but you can still nominate someone. Your FRA would then take your wishes into account when making their decision.

The easiest way to nominate your beneficiary is via PensionPoint.

In addition to the death grant, if you die in retirement, your loved ones may be eligible to receive a pension if they qualify as your surviving spouse, civil partner or cohabiting partner. It would be paid to them for the rest of their life even if they re-married or entered a new partnership. The amount they receive would usually be half your annual pension.

Please note – if your partner is more than 12 years younger than you, their pension would be reduced to reflect the age difference up to a maximum of 50%.

As well as a survivor’s pension, your surviving partner (including civil or cohabiting partner) would receive a bereavement pension (equal to your full pension) for the first 13 weeks after your death. If you don’t have a surviving partner, your child(ren) would be eligible.

Your pension could also provide financial security for your child(ren) if they meet certain qualifying conditions. Depending on their circumstances, children’s pensions are usually paid up to age 18 or age 23 if they are in full time education.

For more details, please speak to your FRA or see the Firefighter scheme guide.

1987 scheme

1. Survivor’s adult pension

If you die in retirement, your loved ones may be eligible to receive a pension if they qualify as your surviving spouse or civil partner (excluding cohabiting partner). This will be paid for the rest of their life but would stop if they re-married or formed a new civil partnership.

The amount they would receive depends on when you joined the scheme:

Before April 1972: the amount payable is based on whether you opted to up-rate the pension you built up before April 1972 (eg by paying additional pension contributions or taking reduced pay).

After 1 April 1972: the amount payable is half your annual pension.

If you married after retirement, the amount would be based on your service after 5 April 1978 only.

Short-term increase

For the first 13 weeks after your death, your spouse’s or civil partner’s pension will be increased so that it is equal to your weekly pension (including any child allowances payable).

2. Children’s pension

Your pension could also provide financial security for your child(ren) if they meet certain qualifying conditions. Depending on their circumstances, children’s pensions are usually paid up to age 16 or age 23 if they are in full time education.

For more details, please speak to your Police Authority or see the 1987 Gov scheme guide.

2006/2015 scheme

If you die within two years of receiving your pension (before age 75), your beneficiaries may receive a one-off lump sum. This is known as a two-year guarantee period. The amount is calculated based on the difference between the pension payments already paid to you and the total amount that would have been paid in the first two years of retirement.

Nominating beneficiaries

Your Police Authority has the power to decide who will receive the death grant but you can still nominate a person(s) via PensionPoint

Or download a nomination form and send it to us via our online contact form or by post.

If you die in retirement, your loved ones may be eligible to receive a pension if they qualify as your surviving spouse, civil partner or declared partner, which would be paid to them for the rest of their life. The amount they receive would usually be half your annual pension. Although, if your partner re-married within six months before your death, the Police Authority may decide not to give them a survivor’s pension.

Please note – if your partner is more than 12 years younger than you, their pension would be reduced to reflect the age difference up to a maximum of 50%.

Your pension can also provide financial security for your child(ren) if they meet certain qualifying conditions. Depending on their circumstances, children’s pensions are usually paid up to age 19 or age 23 if they are in full time education.

This is a separate benefit from the Police Pension Scheme. If you die within 12 months (2006/2015 scheme) or within two years (1987 scheme) of retiring because of an injury sustained while on duty, your surviving spouse or dependent may be eligible to receive an injury death payment.

For more details, please speak to your Police Authority or see the Police scheme guide.